Week 2️⃣ 6️⃣

Premflix

🔊 Audio

📜 Show transcript

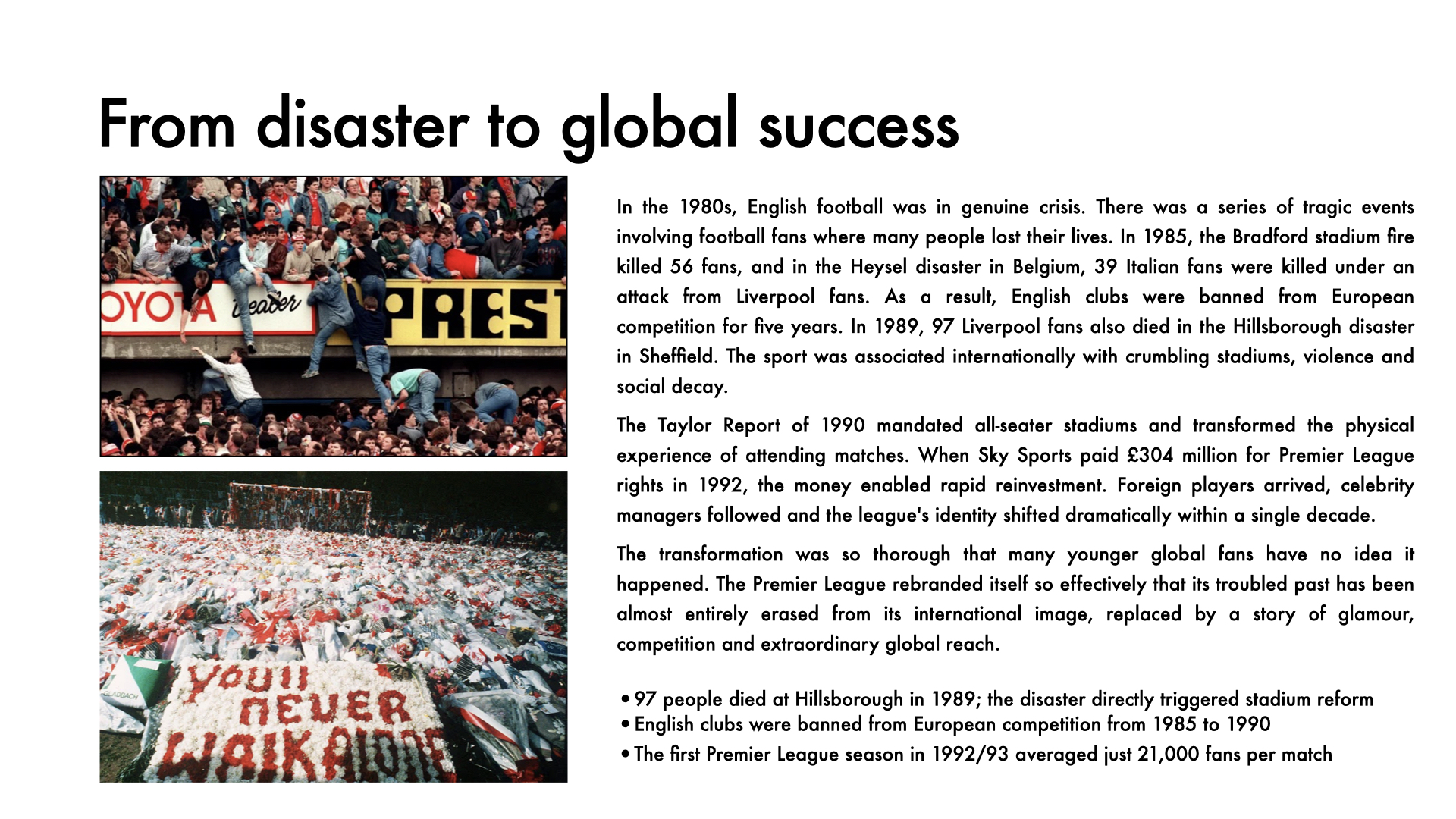

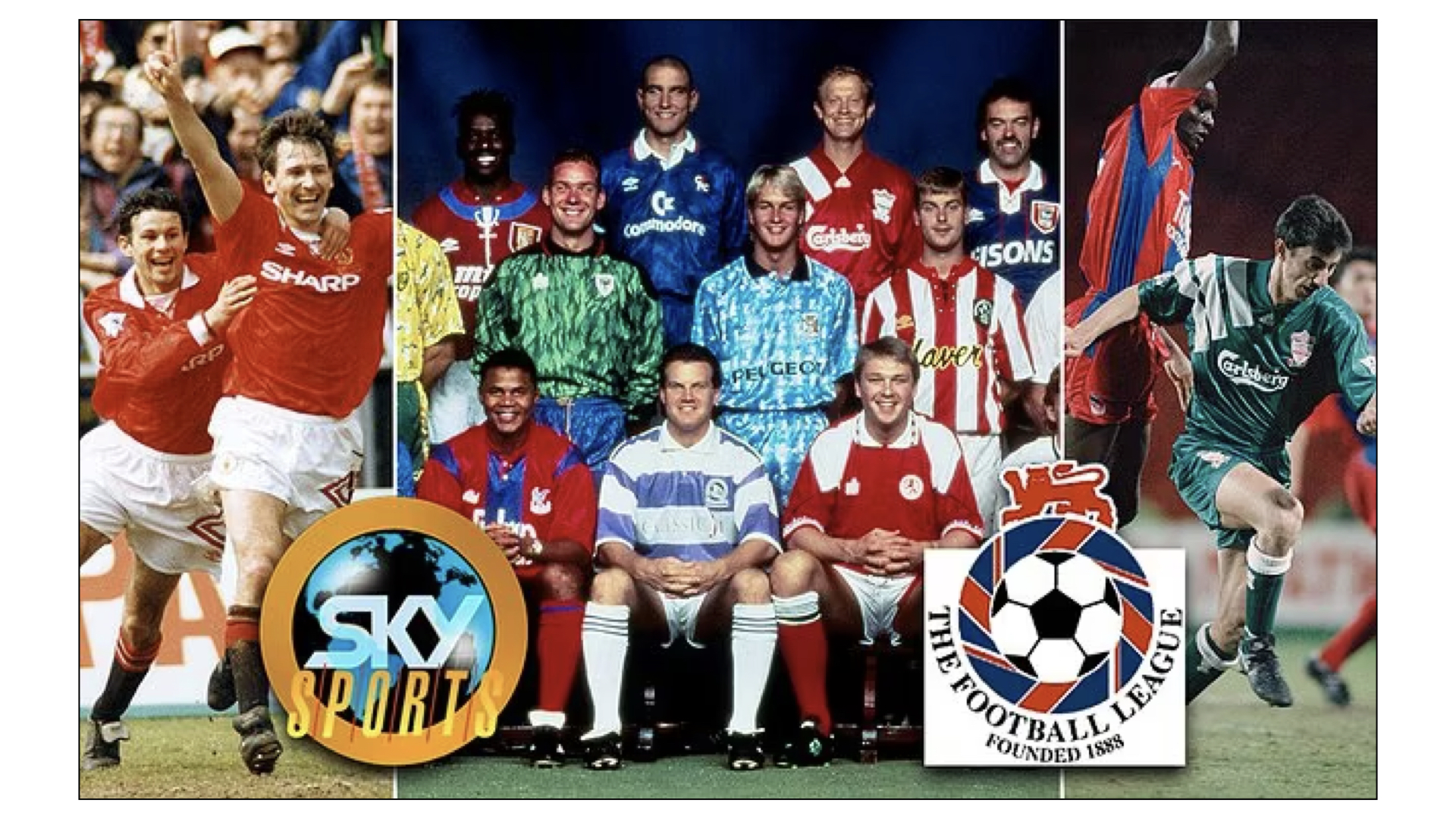

Thirty years ago, English football was rebuilding itself. Hillsborough, Heysel, Bradford: the 1980s had been a decade of tragedy, violence and crumbling stadiums. Then came the Taylor Report, the birth of the Premier League and a cheque from Sky Sports, and everything changed. Within a decade, English football had reinvented itself as a global entertainment product.

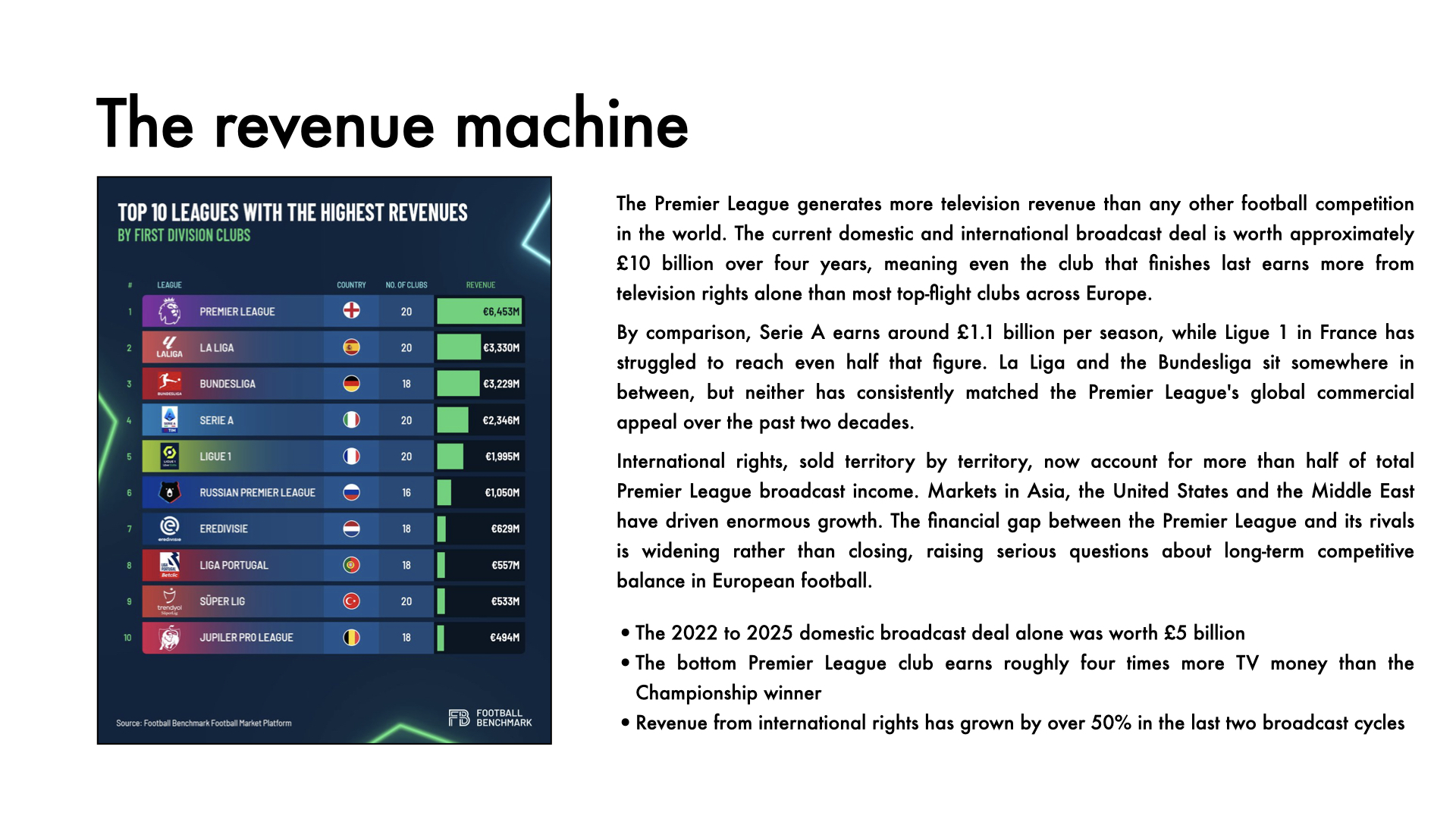

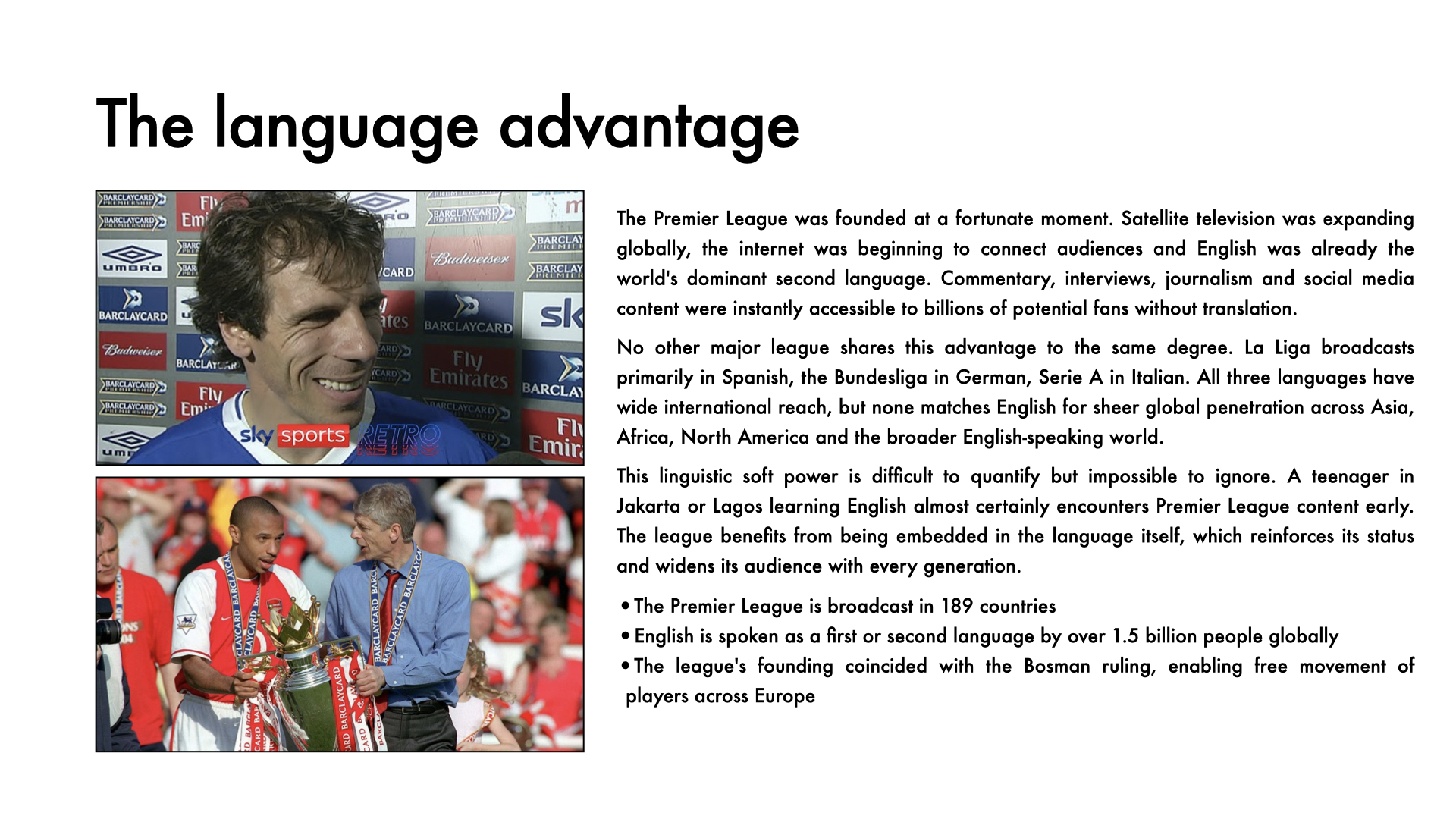

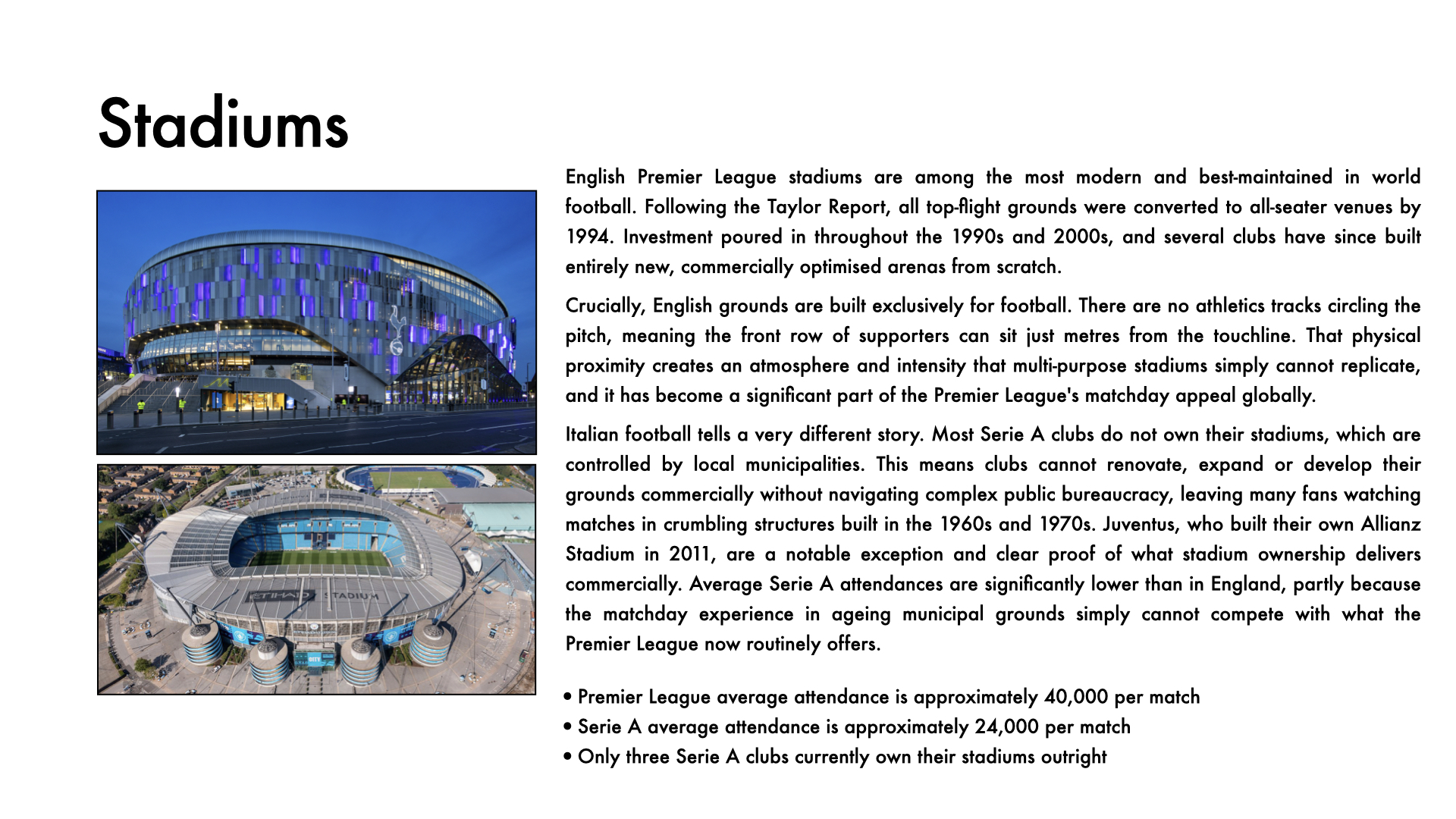

Today the Premier League is broadcast in 189 countries, generates more television revenue than any other league, and benefits from something few rivals can replicate: the English language. From Buenos Aires to Beijing, fans have grown up watching in the language they were already learning at school. Combined with modern all-seater stadiums built purely for football, where fans sit close to the pitch, this has helped create an atmosphere and global reach that Serie A, the Bundesliga and Ligue 1 have struggled to match.

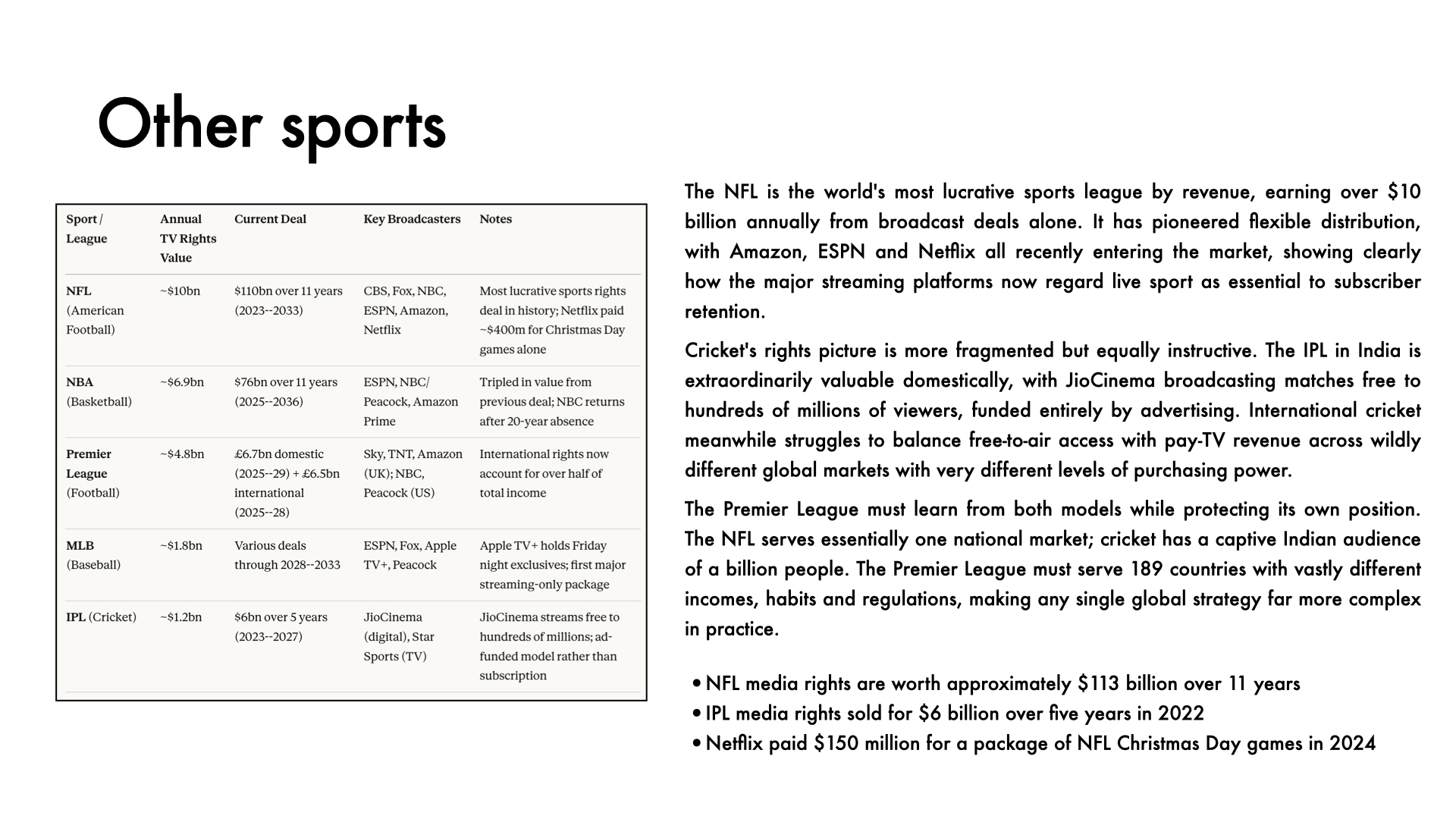

But the model behind this success, selling rights to broadcasters like Sky, DAZN and NBC, is beginning to look vulnerable. The streaming revolution has changed the logic. Netflix sells directly to over 300 million subscribers. The NFL has deals with Amazon and Netflix, while cricket’s IPL streams free to hundreds of millions, funded by advertising. The question is simple: why keep the middleman?

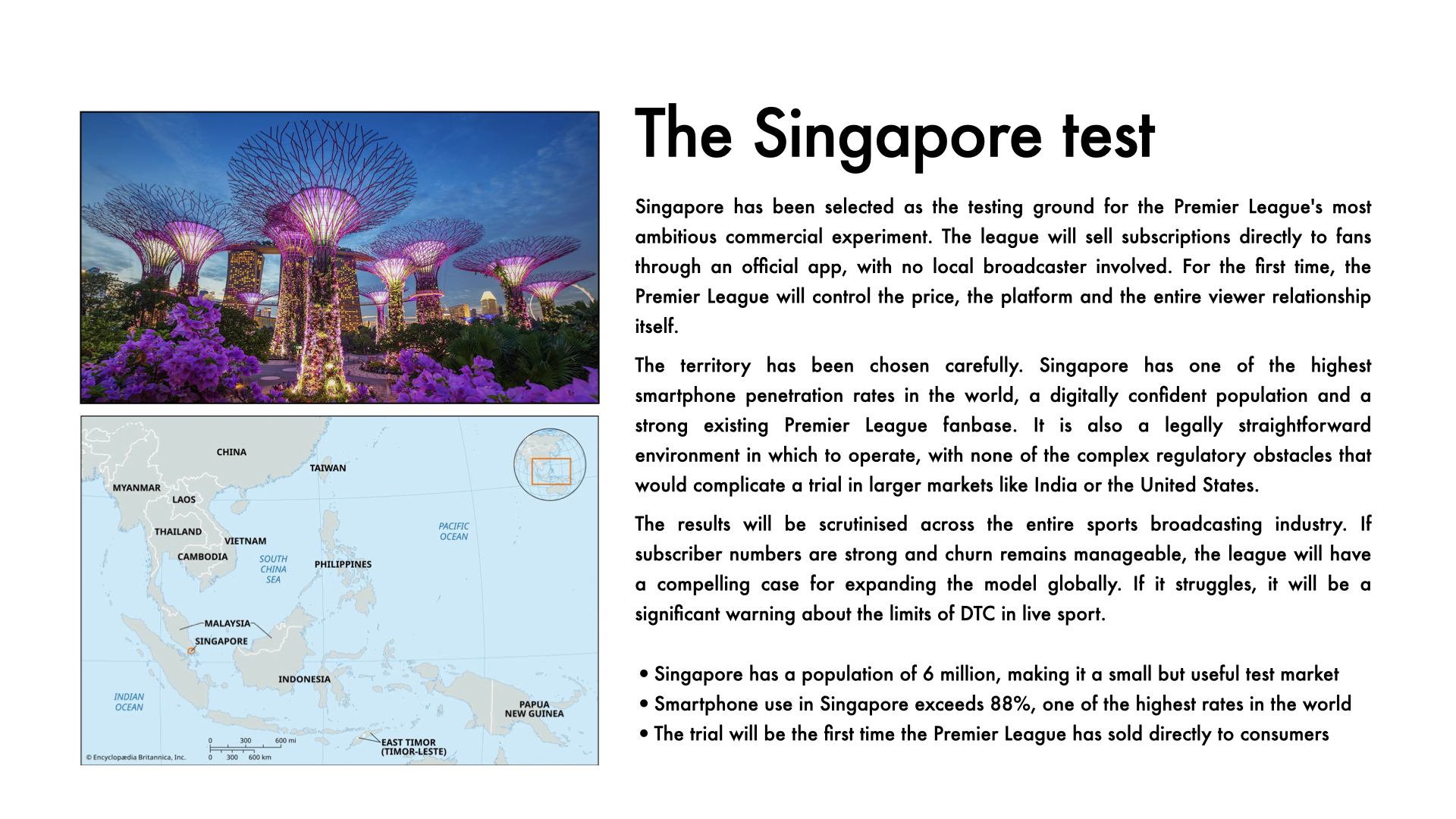

A direct-to-consumer Premier League service, Premflix, is no longer theoretical. Singapore has been chosen as a test market. But as Disney discovered, going direct is harder than it looks. Pricing a global service across countries with vastly different incomes is complex. Keeping subscribers engaged through the off-season is another challenge. Building the infrastructure that broadcasters have spent decades refining is neither quick nor cheap.

The French league’s near-collapse after the Mediapro deal showed what happens when broadcast revenue disappears. Premflix could be the future, or a costly lesson. That uncertainty is what makes it so compelling.

📽️ Slideshow

📺 Video

🔑 Key Vocabulary

- Ad-supported tier – a cheaper or free streaming option where viewers watch adverts instead of paying a full subscription fee.

- Broadcast rights – the legal permission to transmit a sporting event on television, radio or online platforms.

- Bundling – packaging several products or services together and selling them as a single combined offering.

- Churn – the rate at which subscribers cancel a service over a given period.

- Direct-to-consumer (DTC) – a model in which a producer sells directly to the end user, cutting out intermediaries such as broadcasters.

- Exclusive rights – a contract giving a single broadcaster sole permission to show specific content, blocking all competitors.

- First-party data – information collected directly from a company's own customers, considered more valuable than data bought from third parties.

- Gatekeepers – established companies, such as traditional broadcasters, that control access to audiences.

- Geoblocking – restricting online content to users in specific countries, commonly used to enforce territorial broadcast agreements.

- Lateral competition – rivalry between services offering different content but competing for the same consumer time and money.

- Market penetration – the extent to which a product has been adopted by consumers within a given territory.

- Middleman – a company acting as an intermediary between a producer and the end consumer.

- Price sensitivity – the degree to which consumers change their buying behaviour in response to price changes.

- Purchasing power parity – the idea that prices should reflect what consumers in different countries can realistically afford.

- Revenue share – an arrangement in which income from a deal is divided between two or more parties according to an agreed formula.

- Rights holder – the organisation that legally owns the rights to a competition and controls how it is distributed and sold.

- Solidarity payments – funds distributed by a league to smaller or lower-division clubs as a share of centrally negotiated broadcast income.

- Streaming – delivering video or audio content over the internet in real time, without downloading a file in advance.

💬 Conversation Questions

- Do you currently pay for a streaming service? How many do you subscribe to, and do you feel you get good value?

- Have you ever cancelled a subscription and then resubscribed a few months later? What made you do it?

- How do you usually watch Premier League football? Through a broadcaster, a pub, a stream, or something else?

- Would you pay directly for a Premier League app, or would you only watch if it were included in a package you already have?

- Do you think the 3pm Saturday blackout is a good rule or an outdated one? Does it affect you personally?

- The Premier League earns far more from TV rights than Serie A or Ligue 1. Does that feel fair to you, or does it damage European football overall?

- Disney spent billions on streaming and still struggled. Does that surprise you? What does it tell us about the limits of big brands?

- If you lived in Singapore, would you be an early adopter of Premflix, or would you wait to see how it developed?

- Do you think promotion and relegation makes football more exciting, or does the uncertainty make it harder to follow a club long-term?

- If you could redesign how football is broadcast from scratch, what would your ideal model look like?